Table of Content

A mortgage is a loan used to purchase or maintain real estate. These loans are typically in areas designated as rural by the USDA. Borrowers must meet income eligibility limits based on the median income of their county and their household size.

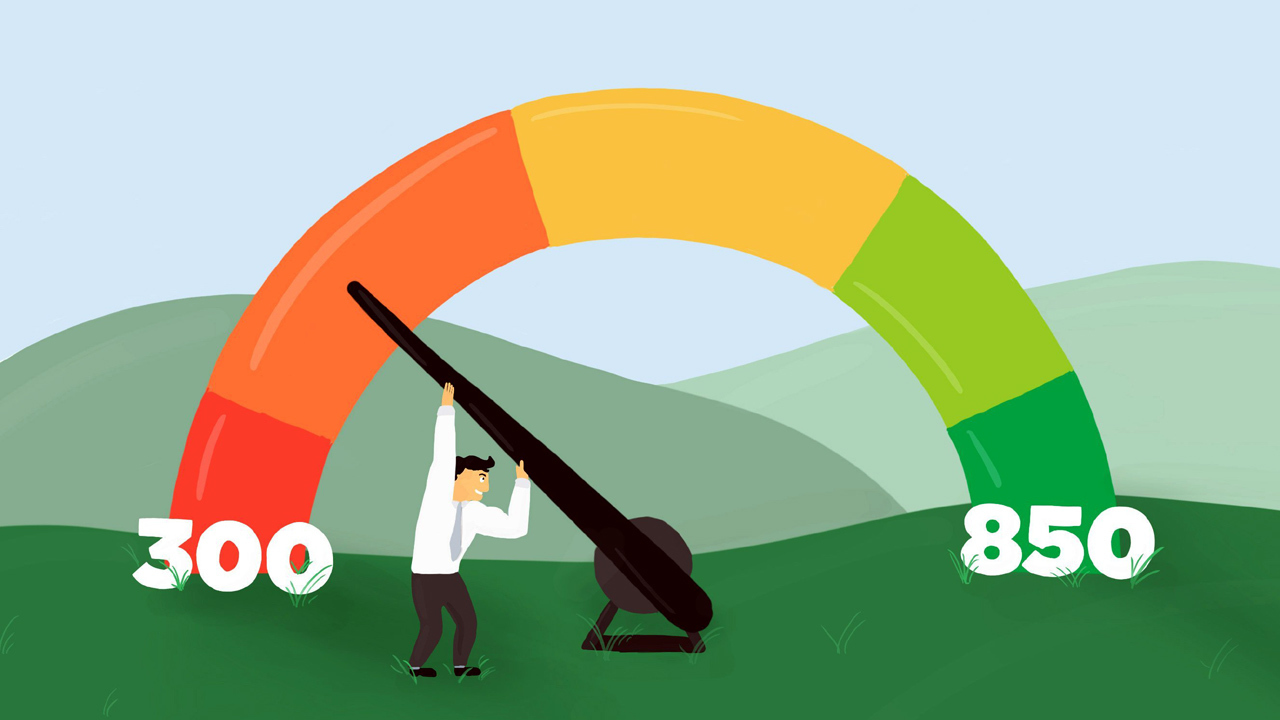

A more accurate definition of the score ranges would be; 300 to 579 is considered poor, while 580 to 669 is given a fair rating. Obviously, the first thing to focus on would be to obtain a good credit score. Moreira Team is a boutique mortgage broker and lender built to cater towards your financial needs, finding the best loan for your unique situation. We believe in a consultative “done-for-you” approach to getting a mortgage.

Pay your bills on time, every time

And they may not impact the specific credit scoring model that your lender is using, but, still, alternative data is a potential option to explore. You’ll have to decide whether the monthly fee is worth a credit score bump. Credit missteps won’t necessarily stop you from becoming a homeowner. Get advice from a housing counselor and work on improving your finances. If you don’t know your credit score, check your most recent credit card statement. Many major credit card companies now provide credit scores for all customers on a monthly basis.

It usually takes less than 30 – 45 days to see the effects of adding bulk, new accounts to your report. When it comes to the actual number, anything less than a 670 FICO® Score is considered “bad” or “subprime,” according to Experian™, one of the three main credit bureaus. More specifically, a fair score is 580 to 669, while a poor score is 300 to 579.

Featured Articles

In addition, the government guarantees the loan and helps with closing costs. Of course, the best option is to work on repairing your credit score before you submit a mortgage application. While this is not the answer borrowers want to read or hear, it’s the most practical and can save you thousands in interest payments. Not only will you have more mortgage options, but you might be able to get your loan with a lower income requirement and down payment. There isn’t a set minimum requirement for income, credit score or down payment to qualify for a conventional loan.

You may qualify for a conventional loan, which isn't backed by a government agency like the FHA or VA, with a minimum credit score of 620. Of course, maybe you just haven’t borrowed much money, or you don’t have a portfolio of different types of credit. That can result in a low score even though you haven’t been irresponsible with credit cards. But to lenders, that’s a risk to them because they don’t have evidence for well-managed borrowing behavior. While it’s true that all lenders are a little different, it’s standard for interest rates to be based largely on the range of your credit score.

NY Times Best Seller

When you choose your lending institution, you’ll want to get a pre-approval letter. The preapproval letter will show the home owner you want to purchase that the chances are excellent you’ll get the loan. Some things you may want to consider when selecting a mortgage include the interest rate, the terms of the loan, and whether or not you will need to make any down payments.

Not only that, but many people who would otherwise be able to afford a mortgage can’t seem to qualify for one. After the 2008 financial crisis, banks made lending requirements much more strict to prevent a housing catastrophe from ever happening again. This is most often referred to as your “average age of accounts” and is one of the few factors you have almost no control over. Your credit history is basically the age of your oldest credit account, new credit accounts and the average ages of all the accounts on your credit report.

It also signals to other lenders that you are not efficient at managing your debt and that’s why you continuously need to keep borrowing. Department of Housing and Urban Development to provide consumer housing counseling. The mission of HUD is to create strong, sustainable, inclusive communities and quality affordable homes for all.

But, if you can’t qualify for a mortgage today and you want to get into the real estate market, this may be a good option for you. Call up real estate agents in your area and ask if they know any sellers willing to provide owner financing. You should also tell them to let you know if they come across sellers looking to provide financing.

While this may not be the “official” score used by a mortgage underwriter, it should give you a good idea of where you stand. A score of 620 may be enough to land a conventional loan, especially if you have a high income or offer a down payment of 10% or more. If you're approved for a conventional mortgage with a fair credit score, you may end up with a higher interest rate than is currently advertised. Additionally, the averaging of credit scores doesn't apply to every loan option. If you have bad credit and fear you’ll face a loan denial when applying for a mortgage, don’t worry.

When you do pay off the collection, it still can remain on your report shown as paid. While this is better than having outstanding debt, it isn’t ideal. If you can either get more available credit or pay down your credit balance, you will improve your utilization. Since this makes up a large part of your score, it should have a positive effect fairly quickly. If you have a score under 600, you are probably limited to an FHA loan, which otherwise might not offer the best deal.

If you buy a Fannie Mae backed home, new rules started in 2017 allow you to buy a home with as little as 5% down. Again, you must pay PMI until you’ve paid off another 15% of the mortgage, but it drops off. Now you can qualify as long as your DTI is between 45% and 50%. Owner-financed homes are not always easy to find, especially when the housing market is hot.

No comments:

Post a Comment