Table of Content

Generally speaking, you'll need a credit score of at least 620 in order to secure a loan to buy a house. That's the minimum credit score requirement most lenders have for a conventional loan. With that said, it's still possible to get a loan with a lower credit score, including a score in the 500s. A good credit score typically means you’ll get a great mortgage. A bad credit score means you’re in trouble, but you shouldn’t just throw in the towel. From low credit score mortgages to cash options to down payment strategies, this crash course explains how to buy a home with bad credit.

You may still be able to get a mortgage with a low credit score. Of course it will depend on a few factors, so your best bet to see if you’ll qualify for a loan is to talk to a lender. Many lenders will have a conversation with you about your eligibility with no obligation to apply for a loan.

Five ways to buy a house with a lower credit score

However, you have to prove that you are not a potential defaulter. Your score still matters, but you are still likely to be approved if it is not below 580. To see scores for mortgages, you can purchase a full report from myFICO.com. The most economical approach is to sign up, download the first month’s information, then cancel the service before the next billing cycle.

Even if you have reversed the downward spiral of your credit history, you might need to tell a prospective lender that there may be some signs of bad credit in your report. This will save you time, since he or she will look at different loans than he might otherwise. An FHA mortgage is often an excellent place to start as they have lower credit score requirements than some other mortgage programs. Improving your debt-to-income ratio can also help you get approved for a mortgage with bad credit.

Pay off other debts.

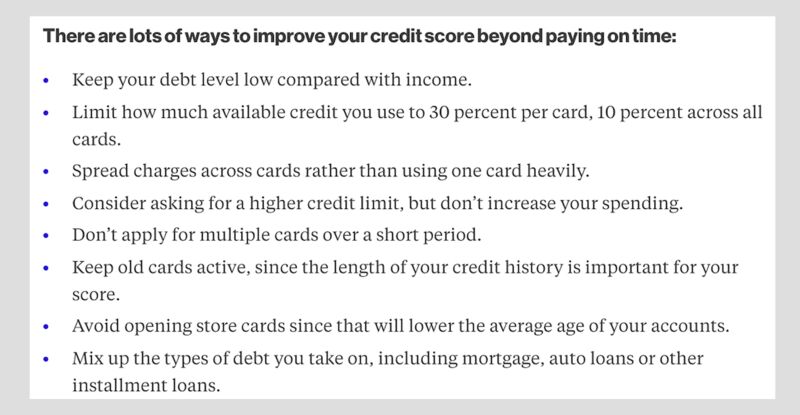

Just changing one of these components of your spending behavior can positively affect your credit score. In other words, to a mortgage lender, there’s no such thing as bad credit. There is only qualifying credit, which is the minimum score required to approve a mortgage application. A home loan can actually help raise your credit score in the future. All you need to do is make sure you make all payments on time and pay off your other debts. After you have increased your credit score, you may have the opportunity to refinance your home and obtain a lower interest rate and payment.

If this will help your credit score, you should ask to have this agreement made in writing so you can make sure it is removed when you pay. If you have a collection on your credit report, lenders aren’t going to be convinced you’ll be a reliable borrower. The collection shows you haven’t paid back the money you owe and haven’t attempted to deal with the debt. Thanks to the hit from the inquiries, you shouldn’t do this immediately before applying for a mortgage. It can also take 1 to 2 months for the effects of adding more credit accounts to show themselves in your score.

How to prepare your credit score for a mortgage?

In addition to being recognized as one of the best real estate blogs, Kyle has been recognized as one of the top Realtors on social media by several organizations and websites. Sign up for a credit improvement service such as Credit Karma or Credit Sesame. Both are excellent companies that can speed up improving your credit standing. Speak to your mortgage broker or loan officer to see if they agree it would be the best program. Alt-A is a classification of mortgages with a risk profile falling between prime and subprime.

If you have a credit score of 680, the maximum amount you can borrow for a personal loan is $100,000. $100,000 is the maximum loan amount for personal loans no matter what your credit score is. If you are trying to find a bad credit lender nearby do a Google search. Up next and making up around 30% of your credit score is how much of your available credit you are using.

Q:June 21, 2022Can I buy a house with a 500 credit score?Meghan Alard

You’ll love these tips on using bad credit home loans when buying a house. A mortgage lender will examine the co-signer’s credit, income, DTI, and more during the application process. Using a co-signer means that you and that individual will have equal share in the house you purchase. If you get into financial difficulties and cannot make your payments, your co-signer will be legally responsible for the debt. Look for potential errors, such as accounts that may not belong to you or inaccurately reported late payments.

This is basically extra money added to your monthly mortgage payment. You pay until you’ve paid off 20% of the home’s value; then PMI drops off and your payments will be reduced. That means the USDA will step in and cover the debt if you stop making payments. The house would still face foreclosure, but the government promises to make the lender whole. If you're interested in buying a home in a qualifying rural area with no down payment, a USDA loan makes it possible with a score in the 640 range. FHA home loans are backed by the Federal Housing Administration and typically require a credit score of around 580.

Keep this in mind when improving your scores and doing a refinance. Even though you are already applying for a loan, you should be working toward improving your credit standing. By improving your credit score, you can refinance at some point in the future into more favorable terms.

Even if you have low credit, there are still options for buying a home. Among other qualification requirements, mortgages will have credit score requirements. The minimum credit score you’ll need depends on the loan type.

If you have a better income or can pay a higher down payment, a conventional loan could be a better option. If you can meet those requirements, you could even get away with a lower credit score. If you don’t qualify for any government-backed programs, you can still get a conventional loan with bad credit.

The course contains information about budgeting, borrowing, and everything buyers need to know before they sign the paperwork on their new home. If you’re in doubt, ask a lender for a quote or use an online quote comparison tool to get several quotes. This will help you judge where rates are and what you can qualify for now that your score is higher.

Pull your credit report to see why your credit is low and check for errors. This is free to do once a year from Equifax, Experian, and TransUnion at AnnualCreditReport.com. Get started today and formulate your plan with an online pre-approval. It’s never too early to get started, and it sometimes can be too late. If you have student loan debt, you may be wondering how this affects your ability to buy a home.

No comments:

Post a Comment